IgA Nephropathy Market Forecast to 2036: Novel Therapies and Key Growth Drivers Fuel Expansion | DelveInsight

The IgAN market is growing due to rising prevalence, improved diagnostics, novel immunotherapies, ongoing clinical trials of therapies such as Zigakibart (Novartis), Sefaxersen (F. Hoffmann-La Roche/Ionis Pharmaceuticals), Povetacicept (Vertex Pharmaceuticals), ULTOMIRIS (AstraZeneca), Atacicept (Vera Therapeutics), Felzartamab (Biogen), TAK-079 (Takeda Pharmaceutical), WAL0921 (Walden Biosciences), ARO-C3 (Arrowhead Pharmaceuticals), and others, increased awareness, and strong R&D investment, driving advances in treatment and early detection.

New York, USA, April 29, 2026 (GLOBE NEWSWIRE) -- IgA Nephropathy Market Forecast to 2036: Novel Therapies and Key Growth Drivers Fuel Expansion | DelveInsight

The IgAN market is growing due to rising prevalence, improved diagnostics, novel immunotherapies, ongoing clinical trials of therapies such as Zigakibart (Novartis), Sefaxersen (F. Hoffmann-La Roche/Ionis Pharmaceuticals), Povetacicept (Vertex Pharmaceuticals), ULTOMIRIS (AstraZeneca), Atacicept (Vera Therapeutics), Felzartamab (Biogen), TAK-079 (Takeda Pharmaceutical), WAL0921 (Walden Biosciences), ARO-C3 (Arrowhead Pharmaceuticals), and others, increased awareness, and strong R&D investment, driving advances in treatment and early detection.

IgA nephropathy is the most common primary glomerular disease worldwide and a leading cause of chronic kidney disease, characterized by IgA immune complex deposition in the kidneys that drives inflammation, proteinuria, and progressive renal damage.

Treatment has shifted from traditional supportive care focused on blood pressure control and proteinuria reduction with ACE inhibitors, ARBs, and SGLT2 inhibitors to targeted disease-modifying therapies. Approved agents now include FABHALTA, VANRAFIA, TARPEYO/ KINPEYGO, FILSPARI, and VOYXACT. Most recently, VOYXACT received US FDA approval as the first APRIL-blocking therapy, offering a novel option to reduce proteinuria and slow disease progression.

Reflecting continued innovation, the late-stage IgAN pipeline features Phase III candidates such as BAFF/APRIL dual inhibitors povetacicept and atacicept, anti-CD38 antibodies felzartamab and mezagitamab, complement inhibitors ravulizumab and ARO-C3, anti-APRIL therapy zigakibart, and the gene-silencing candidate sefaxersen. These biologics, monoclonal antibodies, and RNA-based therapies are expected to further expand treatment options and reshape long-term disease management.

Discover which segment will drive growth in the IgAN market @ https://www.delveinsight.com/sample-request/iga-nephropathy-igan-market

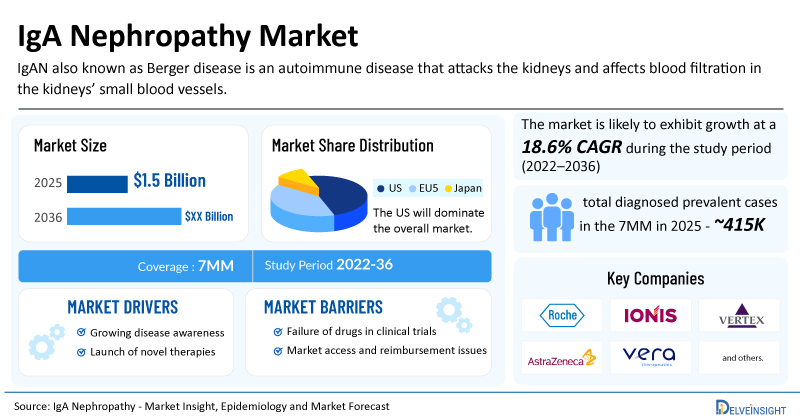

The IgAN market across the 7MM was valued at USD 1.5 billion in 2025 and is projected to grow at a marvellous CAGR of 18.6% through 2036, driven by rising prevalence, expected launch of therapies, and strong R&D investment driving advances in treatment and early detection. Let’s discuss these market drivers in detail.

Key Factors Driving the Growth of the IgAN Market

- Rising Prevalence of IgAN: IgAN is one of the most common primary glomerular diseases worldwide and remains a leading cause of CKD and ESRD. The total diagnosed prevalent cases of IgAN across 7MM is found to be approximately 415K in 2025. This number is expected to rise in the coming years.

- Growing Need for Effective Targeted Therapies: Conventional treatment with ACE inhibitors, ARBs, and SGLT2 inhibitors mainly addresses symptoms and slows progression but does not directly target disease biology. A significant proportion of patients continue progressing to chronic kidney disease or kidney failure, driving demand for more effective precision therapies.

- Recent Launches of TARPEYO and FILSPARI: The recent launch of innovative drugs like TARPEYO and FILSPARI will fuel the market growth.

- Higher Healthcare Spending and Rare Disease Focus: Governments and payers are increasingly prioritizing chronic kidney disease prevention due to the high cost of dialysis and transplantation. Treating IgAN earlier with branded therapies can reduce long-term renal replacement costs, supporting reimbursement.

- Strong Clinical Trial Activity: The emerging landscape holds a diverse range of therapeutic alternatives for treatment, including Zigakibart (Novartis), Sefaxersen (F. Hoffmann-La Roche/Ionis Pharmaceuticals), Povetacicept (Vertex Pharmaceuticals), ULTOMIRIS (AstraZeneca), Atacicept (Vera Therapeutics), Felzartamab (Biogen), TAK-079 (Takeda Pharmaceutical), WAL0921 (Walden Biosciences), ARO-C3 (Arrowhead Pharmaceuticals), and others in different phases of clinical development. The expected launch of these therapies shall further create a positive impact on the market.

Now, take a look at these emerging therapies in detail that are poised to reshape the future of IgAN management.

Novartis’ Zigakibart

Anti-APRIL

Zigakibart is a subcutaneously delivered monoclonal antibody designed to selectively inhibit APRIL, an important mediator of pathogenic IgA production. The therapy is presently in Phase III clinical trials for IgA nephropathy, with Novartis targeting regulatory filings in 2027. The candidate is supported by a strong intellectual property portfolio that includes several granted U.S. and global patents, along with more than twenty pending patent applications. These protections span both composition-of-matter and therapeutic use claims and are projected to provide market exclusivity from 2030 through 2041, excluding any possible patent term extensions.

In August 2023, Novartis finalized its acquisition of Chinook Therapeutics in a transaction worth up to USD 3.5 billion. Earlier, in July 2022, the European Commission awarded BION-1301 Orphan Drug Designation for the treatment of primary IgAN.

Ramandeep Singh, Senior Consultant of Forecasting, DelveInsight, said that advancement into multiple Phase III programs, supported by Novartis and strong patent coverage, underscores confidence in its disease-modifying potential and positions zigakibart as a future cornerstone therapy in IgAN.

Vertex Pharmaceuticals’ Povetacicept

Dual antagonist of BAFF and APRIL

Vertex Pharmaceuticals’ povetacicept (ALPN-303) is an advanced dual inhibitor of BAFF and APRIL, two important cytokines involved in autoimmune disease progression through B-cell activation, maturation, survival, and wider immune regulation. Designed with an enhanced TACI domain, povetacicept has shown stronger binding capacity and superior functional activity compared with earlier BAFF/APRIL inhibitors in preclinical studies. These advantages have translated into promising clinical outcomes, including best-in-class efficacy signals in patients with IgAN, highlighting its potential as a differentiated immunomodulatory treatment.

In June 2025, Vertex Pharmaceuticals and Ono Pharmaceutical announced an exclusive collaboration and licensing agreement to co-develop and commercialize povetacicept in Japan. Earlier, in May 2024, Vertex Pharmaceuticals acquired Alpine Immune Sciences for around USD 5 billion, gaining povetacicept as a flagship asset within the deal.

As per Singh, povetacicept (ALPN-303) emerges as a highly differentiated IgAN therapy, delivering deep and durable proteinuria reductions, meaningful Gd-IgA1 suppression, high hematuria resolution rates, and stable eGFR, alongside a favorable safety profile.

Explore what are the emerging therapies in IgAN and their market impact @ Emerging Therapies in IgAN Market

Biogen’s Felzartamab

Anti-CD38

Felzartamab is a precision-engineered monoclonal antibody that targets CD38, a surface protein abundantly found on mature plasma cells. Through the selective elimination of CD38-expressing plasma cells, it is designed to reduce the production of harmful autoantibodies responsible for immune-driven kidney damage. This mode of action supports felzartamab’s potential as a disease-modifying therapy for IgAN, as it focuses on the root cause, antibody-producing cells, rather than only controlling downstream inflammation.

Key clinical readouts are expected between 2028 and 2030. In November 2024, felzartamab received Orphan Drug Designation in Europe for IgAN treatment. Originally developed by MorphoSys AG, the company now operates as MorphoSys GmbH following its acquisition by Novartis in May 2024. Under plans to launch a Phase III study, MorphoSys is set to receive a one-time milestone payment of USD 35 million from Biogen.

Vera Therapeutics’ Atacicept

BAFF and APRIL dual inhibitor

Atacicept is an investigational recombinant fusion protein designed to inhibit BAFF and APRIL, two important cytokines that promote B-cell survival and autoantibody production implicated in the development of IgA nephropathy. Vera Therapeutics completed full enrollment in the pivotal Phase III ORIGIN trial in April 2025, after earlier finishing enrollment for the primary endpoint cohort in September 2024. The ORIGIN 3 study also delivered topline results that support the company’s planned Biologics License Application (BLA) submission. Earlier, in May 2024, the US FDA granted Breakthrough Therapy Designation (BTD) to atacicept for the treatment of IgA nephropathy.

To know more about emerging FcRn therapies to reshape IgAN treatment landscape, visit @ IgA Nephropathy Medication

AstraZeneca’s ULTOMIRIS

Complement C5 inhibitor

ULTOMIRIS (ravulizumab) is an extended-duration monoclonal antibody designed to block the C5 protein within the terminal complement cascade, enabling rapid, complete, and durable complement inhibition. By acting on this pathway, ULTOMIRIS helps reduce excessive immune system activation that may otherwise harm healthy cells. The therapy is currently under investigation in the Phase III ICAN clinical trial for the treatment of IgAN. It is also covered by patent protection in key global markets, with expected expiry in the United States in 2035 (extendable to 2038), in the European Union through 2035 (with extensions to 2038–2040), and in Japan until 2038.

According to Sadaf Javed, Manager of Forecasting and Analytics at DelveInsight, the successful readout of the ongoing ICAN Phase III trial will be critical to confirm durability, risk–benefit balance, and commercial viability in an increasingly competitive IgAN landscape.

F. Hoffmann-La Roche/Ionis Pharmaceuticals’ Sefaxersen

Complement factor B expression inhibitors; gene silencing

Roche and Ionis Pharmaceuticals are jointly developing Sefaxersen (RG6299; IONIS-FB-LRx), an antisense oligonucleotide designed to reduce complement factor B gene expression by targeting factor B mRNA. It is the first ASO aimed at selective complement pathway suppression in IgAN. In July 2022, Roche exercised its option to license IONIS-FB-LRx following positive Phase II results. Roche is now responsible for global development, regulatory, and commercialization activities and associated costs, excluding the open-label Phase II study in patients with IgAN, which remains under Ionis’ conduct and funding.

As per Javed, Roche’s decision to exercise its option and assume global development underscores confidence in the program. With Phase III IMAGINATION data expected in 2026, Javed said, Sefaxersen carries meaningful launch potential around 2030, contingent on confirmation of durability, renal protection, and long-term safety in a large, high-risk IgAN population.

Find out more about which drugs will gain maximum market share in IgAN @ IgA Nephropathy Drug Treatment

Takeda Pharmaceutical’s TAK-079

Anti-CD38

TAK-079 (mezagitamab) is an investigational monoclonal antibody from Takeda Pharmaceutical Company designed to target CD38-expressing plasma cells. By selectively eliminating these cells, the therapy seeks to lower harmful autoantibody production while maintaining overall immune function. This precision-based approach supports its potential as a disease-modifying treatment for immune-mediated disorders, including IgAN, with the goal of delivering effective immunomodulation alongside a favorable safety profile. Based on current clinical development progress, Takeda Pharmaceutical Company is targeting a possible mezagitamab launch between 2027 and 2029, subject to positive clinical trial results and regulatory clearance.

Aparna Thakur, Assistant Project Manager of Forecasting, DelveInsight, commented that if ongoing randomized studies confirm these durability and safety signals, mezagitamab could emerge as a competitive plasma cell–directed therapy in IgAN, particularly for patients requiring sustained disease control beyond conventional anti-proteinuric strategies.

Arrowhead Pharmaceuticals’ ARO-C3

Complement C3 inhibitors; RNA interference

ARO-C3 is being developed to reduce the production of complement component 3 (C3) in hepatocytes for the treatment of complement-mediated kidney disorders. Dysregulated complement system activity can contribute to disease progression and tissue injury. By targeting C3 expression, ARO-C3 may help control complement cascade activation, representing a promising strategy for managing these diseases.

Walden Biosciences’ WAL0921

Urokinase plasminogen activator receptor antagonists

WAL0921 is a first-in-class anti-suPAR antibody developed to neutralize soluble urokinase plasminogen activator receptor (suPAR), a circulating pro-inflammatory protein linked to the development and progression of kidney disorders such as Focal Segmental Glomerulosclerosis. Increased suPAR levels are associated with podocyte damage and proteinuria through activation of harmful signaling pathways. Both preclinical and clinical studies indicate that lowering suPAR levels through antibody inhibition or plasmapheresis may help slow or stop disease progression. By addressing the underlying disease driver directly, WAL0921 represents an innovative treatment strategy for suPAR-driven glomerular disorders.

Discover more about IgAN drugs in development @ IgA Nephropathy Clinical Trials

Source: IgA Nephropathy Market Report

IgA Nephropathy Market Insights, Epidemiology, and Market Forecast – 2036 report delivers an in-depth understanding of the disease, historical and forecasted epidemiology, as well as the market trends, market drivers, market barriers, and key gMG companies, including Novartis, Vertex Pharmaceuticals, Biogen, Vera Therapeutics, AstraZeneca (Alexion Pharmaceuticals), F. Hoffmann-La Roche, Ionis Pharmaceuticals, Takeda Pharmaceutical, Arrowhead Pharmaceuticals, NovelMed, Walden Biosciences, Kira Pharmaceuticals, Purespring Therapeutics, Biohaven Therapeutics, and others.

About DelveInsight

DelveInsight is a leading Business Consultant and Market Research firm focused exclusively on life sciences. It supports pharma companies by providing comprehensive end-to-end solutions to improve their performance. Get hassle-free access to all the healthcare and pharma market research reports through our subscription-based platform PharmDelve.

Contact Us Shruti Thakur info@delveinsight.com +14699457679 www.delveinsight.com

![]()

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.